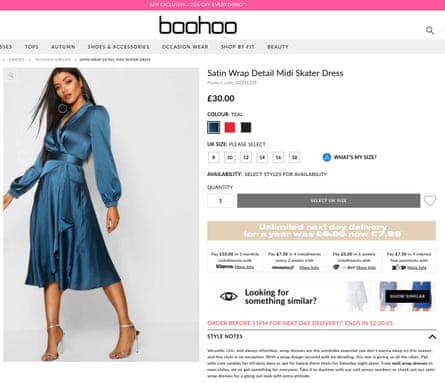

Shoppers tempted by Boohoo’s bestselling satin skater dress are bombarded by options to pay for it using today’s hottest form of consumer credit – “buy now, pay later”.The fast-fashion website gives shoppers four ways to pay for the £30 dress in instalments: from three monthly payments of £10 with Klarna, to six weekly lots of £5 with Laybuy. Even those trying to buy it outright using a debit or credit card see reminders of “more ways to pay” flash up.

Once a niche form of credit, buy now, pay later (BNPL) deals have exploded during the pandemic. Labelled by some as “the future of millennial finance”, it has gained a foothold among the under-30s and those with tight finances, who have welcomed the ability to delay payment for goods, typically without interest. But it has also stoked fears that the unregulated financial product is encouraging unsustainable spending and reliance on debt.

Fintech upstarts – such as Clearpay, Laybuy and industry leader Klarna – have dominated the burgeoning sector, doling out credit to consumers in return for lucrative commission from beauty, fashion and furniture retailers. Last week Monzo became one of the first UK banks to begin rolling out a BNPL service to its 5 million-plus customers, who can use it for online and in-person purchases at any retailer, and secure credit limits of up to £3,000 after an affordability check. Rival Revolut confirmed it was “at the early stages” of developing a BNPL feature for Europe.

Quick Guide

The UK’s leading buy now, pay later players

Show

Klarna

The largest of the providers, Klarna is best known for hiring celebrities such as Snoop Dog and Madonna to advertise its services. The Swedish firm became one of the world’s most valuable fintech companies, second only to Stripe, after it was valued at nearly $46bn (£33bn) earlier this year.

Laybuy

The New Zealand-based firm was launched in 2017 but has grown rapidly across the UK and Australia. Purchases are usually spread across six weekly instalments, and this can also apply to items bought in store at partner retailers. Laybuy runs hard credit checks on customers and says it rejects a quarter of all the people who apply.

Clearpay

This Australian company launched in 2014, and entered the UK two years ago. Known as Afterpay in some countries, it allows customers to pay in four instalments two weeks apart. Clearpay currently only operates online but is hoping to launch in bricks-and-mortar stores by early 2022. It was acquired by San Francisco-based Square in August in a $49bn all-stock deal.

Paypal

The American payments giant allows UK shoppers to split their payments into three monthly instalments at the checkout. It announced in August that it was scrapping late fees for missed payments on all BNPL products globally, which suggests that shoppers had been put off by providers who charged.

Photograph: Thiago Prudencio/Rex FeaturesWas this helpful?Thank you for your feedback.

Mainstream banks are jostling for a slice of the action amid predictions that by 2026, Britons will be spending close to £40bn a year by this method. Traditional lenders may have no choice but to join the goldrush: the boom in BNPL risks cannibalising their lucrative credit card businesses.

Last week, Goldman Sachs spent $2.2bn (£1.6bn ) to acquire GreenSky, a BNPL fintech focused on spreading the cost of home improvement loans rather than retail.

Barclays has said it hopes to extend an existing BNPL venture – which charges interest – and offer credit to Amazon’s UK customers at the checkout. That potential deal is still in the works, but whether the lender will stick with traditional BNPL or scrap interest to rival the upstarts is unclear. Barclays is also partnering with a US fintech to offer “financing instalment options” across the pond. There is also speculation that other UK high street banks are eyeing interest-free BNPL with far broader applications.

For retailers, the lure of BNPL is simple: customers spend more. “It increases the basket size and it also reduces dropped baskets,” said an investor in a BNPL startup. “After a while, if everyone uses it, you would be a brave as a retailer to take it out. If you’re a director of retailing you would say it’s great. But if you were the chief executive of a retailer and looked at it, you would realise it’s a problem.”

Retailers happily pay lenders generous commission in return for those higher sales. The investor said double-digit commission rates were not uncommon in the industry. For lenders, handling payments has shifted from a cost centre to a profit centre, they said.

View image in fullscreenBoohoo’s skater dress on its website, show several payment options. Photograph: Boohoo

View image in fullscreenBoohoo’s skater dress on its website, show several payment options. Photograph: Boohoo

“The issue is the checkout button. That’s the hippy crack of the industry. It’s the button where somebody can pay and leave the checkout without spending any money up front.

“People are signing up to a credit agreement and you cannot say they have fully understood the funding if it’s a two-click process. Nobody reads the terms and conditions.”

Gary Rohloff, co-founder of Laybuy, said it used “hard credit checks” and rejected 25% of applicants to use Laybuy. “We support regulation and, done correctly, [it] will help raise standards across industry. As more providers enter the market that responsibility message is more vital than ever.”

Lenders who decide to jump in will be doing so without knowing what regulations are coming down the track from the Financial Conduct Authority, which is expected to introduce rules for interest-free BNPL products in late 2022 at the earliest. The lack of formal scrutiny has prompted debt campaigners to warn this could be the next Wonga-style scandal to hit the financial sector. The payday lender went bust in 2018.

Sue Anderson of the debt charity StepChange said: “Buy now, pay later services don’t give individuals enough time or protection to stop, pause and understand the consequences of their purchase. Sometimes this even means people end up using BNPL at the online checkout without actually realising they have signed up.

“Second, affordability checks are only used by some BNPL lenders, and protections against taking out multiple BNPL loans are lacking. Finally, due to a lack of regulation, it’s not clear whether these services are treating customers fairly and in a way that is consistent with other credit products.”

Boohoo said the average customer spend per item using BNPL on its website was “relatively low”, at £11.96. “Like virtually every other retailer in the UK, our website offers a range of payment options to suit the needs of our customers.”

Ronan Dunphy, a banking analyst at stockbroker Goodbody, said the regulators’ approach will be a critical determinant of how large the market could get.

“BNPL clearly resonates with a large cohort of consumers, as evidenced by the rapid growth in the market,” he said. “However, this growth has taken place in the absence of any regulatory constraints and in an environment where it is not always clear if consumers understand the terms of the products.”

In the UK, the use of BNPL nearly quadrupled in 2020, to £2.7bn in transactions, according to official data – still a fraction of the £250bn of outstanding consumer credit debt. Between the start of the pandemic and the end of last year, 5 million people used a BNPL product, an FCA survey found, while the consultancy Capital Economics claimed there were “over 10 million users” in 2020.

Analysts at Juniper Research told the Observer that by 2026, spending via BNPL services will hitwas predicted to reach almost $51bn (£37bn) in the UK alone. Globally it predicts spending will reach $995bn in five years’ time, almost four times the current figure.

I hope the new BNPL regulation will include checks on a customer’s ability to repay if they are taking instalment plansJason Wassell, Consumer Credit Trade Association

Up until now the focus has mainly been on occasional fashion and beauty purchases, and the average amounts borrowed are often relatively small – £65-£75 per transaction, according to the FCA.

Some commentators say this has all been fuelled by advertising slogans inviting people to “shop like a queen” and telling them “don’t wait until payday,” as well as by influencers on Instagram. But according to Capco, a technology and management consultancy, that could all change if supermarkets and other essential retailers come on board. The UK has already seen the launch of Flava, which calls itself a “buy now, pay later online supermarket”. It lets people spread the cost of their grocery shopping, and stocks leading brands such as Heinz and Kellogg’s.

BNPL providers are also increasingly partnering with higher-value retailers selling everything from vacuum cleaners and electric guitars to garden furniture and mattresses, edging closer to essential items that could lure in more-vulnerable customers without the protection of FCA regulation.

It has caught the attention of regulators and politicians, who are becoming increasingly concerned about how easy it is for consumers to buy more than they can afford using BNPL and potentially rack up sizeable debts. Because so much of this market is unregulated, critics say some people are able to take out credit that they otherwise would not be able to obtain.

Rivals to the burgeoning industry are also taking note. Short-term lenders, including payday lenders, that have faced their own regulatory crackdown, are concerned that BNPL has made it harder to assess how much debt consumers are actually shouldering and carry out effective affordability checks. The industry has already been stung by a tsunami of compensation claims by customers who say they were mis-sold loans they could not afford: this led to a collapse of a string of payday lenders including Wonga.

“I hope the new BNPL regulation will include checks on a customer’s ability to repay if they are taking instalment plans,” said Jason Wassell, chief executive of the Consumer Credit Trade Association, which represents short-term and payday lenders. “We need increased visibility of this form of borrowing on credit records. BNPL use is currently invisible and means other lenders are making decisions without seeing the whole picture.”

But regulated banks have another concern on the horizon: how BNPL may be diverting income from other revenue streams such as credit cards and traditional loans.

In July the consultancy firm McKinsey said US banks had been slow to respond to the surge in demand for BNPL and so had lost about $8bn to $10bn in annual revenues to fintechs.

“For credit cards in particular, there is a major threat from buy now, pay later,” said Nick Maynard, lead analyst at Juniper Research.

In June, Klarna launched an app that allows UK users to shop at any online retailer, regardless of whether it has partnered with the firm, and split the payment into three interest-free instalments – eliminating the need to use a credit card.

Laybuy – which lets people pay in six weekly instalments – recently launched a digital card allowing customers to buy now, pay later at selected stores with just a tap of their smartphone instead of using their bank plastic.

McKinsey said the largest BNPL players were steadily building scale with the aim of becoming shopping and banking “super apps” that would enable them to take charge of every aspect of the “purchase journey”. There is already evidence of this happening: Klarna said recently that following a successful test phase, it was rolling out current accounts in Germany so people there could “experience the full end-to-end Klarna experience”.

View image in fullscreenPayPal is another big name to have moved in on the BNPL sector. Photograph: Éric Piermont/AFP/Getty Images

View image in fullscreenPayPal is another big name to have moved in on the BNPL sector. Photograph: Éric Piermont/AFP/Getty Images

BNPL providers typically claim to provide a more transparent and cheaper alternative to credit cards. Samantha Palmer, managing director of Payl8r, another BNPL firm, said that “millennials don’t want credit cards and don’t like banks,” adding that young adults found it hard to get finance because they had not had a chance to build their credit rating.

In the UK, PayPal is one of the biggest financial players so far to muscle in on this market. It launched a BNPL service in October 2020 and has unveiled similar services in the US, Australia and France. PayPal said last week that, globally, it had now processed more than $3.5bn (£2.5bn) in payments.

In February this year the government announced that buy now, pay later would be regulated by the FCA after it ruled there was “a significant risk” of harm to consumers. Many consumers did not view BNPL as credit, so did not apply the same level of scrutiny, and checks by providers tended to focus on the risk for the firm rather than how affordable it was for the customer, the regulator found.

The move means firms will have to conduct proper affordability checks before lending and ensure customers are treated fairly if they struggle to repay. There have been warnings from some MPs that BNPL could be “the next Wonga waiting to happen”.

It could be some time before this all takes effect. The Treasury’s consultation on BNPL is expected to be published before the end of October and, assuming parliament passes legislation, the FCA plans to consult on new rules in 2022. Until then, there are a lot of £30 dresses to sell.